The fight for dental insurance reform is underway, and providers—so far—are on the defensive. But how did we get to a place where most dentists say reform is so badly needed? And what are the barriers blocking big changes from benefiting dentists and patients nationwide?

By Mark Caro

THEY CALLED THEMSELVES the Boston Teeth Party because . . . well, of course they did. This was a dental revolution, after all, the attempted overthrow of a system in which citizens were paying money and not receiving enough in return. This battle wouldn’t be fought in boardrooms or on legislative floors. The Teeth Party would take it directly to the people.

THEY CALLED THEMSELVES the Boston Teeth Party because . . . well, of course they did. This was a dental revolution, after all, the attempted overthrow of a system in which citizens were paying money and not receiving enough in return. This battle wouldn’t be fought in boardrooms or on legislative floors. The Teeth Party would take it directly to the people.

“We have ditched the oppression of the king,” says the movement’s flag bearer, a Somerville, Massachusetts–based orthodontist named Dr. Mouhab Rizkallah. “We have been in our cages, and we said, ‘Enough. We’re going to declare our independence. We’re going to free ourselves from this oppression.’ ”

Dr. Rizkallah came to this fight well-armed. For one, he had deep pockets and a willingness to spend. Perhaps more vital were his drive, passion and crusading sense of justice—as well as his detailed business knowledge and appetite for litigation. He is not shy about taking on the powers that be. For his stalwart defense of his principles—as well as his success at the ballot box—he has vaulted seemingly from out of nowhere to the No. 1 spot on our annual list of the 32 Most Influential People in Dentistry.

“I’m known for that, you know,” he says of his spirited willingness to take on entrenched interests. “I won’t fight for me, but if you’re bullying someone around me, I’m going to come to their aid.”

In his view the bullied, at first, were children on Medicaid encountering insurance roadblocks to needed orthodontic treatment, but the aggrieved came to encompass anyone receiving dental care. What Dr. Rizkallah and his allies perceived was that patients were paying significant sums for their dental insurance but not receiving adequate benefits in return. Instead of their premium payments going back into their care, most of it was being funneled into administrative expenses and executive salaries. The doctor cites the 2019 not-for-profit tax form for Delta Dental of Massachusetts, the Bay State’s dominant dental insurance provider, showing that it spent $177 million on patient care that year and contributed $291 million to its parent company.

“That’s a big deal, right?” Dr. Rizkallah says, incredulous. “They gave away $291 million.”

He ardently wished for a method to help him change that equation so the bulk of insurance revenue would go to the people who paid it in the first place. For a model, he looked to the Affordable Care Act, a.k.a. Obamacare, which had its roots in Romneycare, the health care plan signed into law in 2006 by then-Massachusetts Governor Mitt Romney. The ACA mandates that medical insurers spend a certain percentage of revenue on claims, treatment and quality relative to administrative costs. That figure, known as medical loss ratio (MLR), must be at a national minimum of 80 percent; Massachusetts sets it at 88 percent.

The Affordable Care Act, however, does not apply to dental insurance. Dr. Rizkallah thought it should. So he mounted a campaign to put the matter to a state referendum, something that Massachusetts, unlike most states, enables its citizens to do. His initiative, known as Question 2 on the November 2022 ballot, called for a dental MLR of 83 percent, meaning carriers would have to spend that percentage of revenue on patient care. If they failed to meet that threshold, they would be required to give rebates to the consumers who paid into the system.

“We have ditched the oppression of the king. We have been in our cages, and we said, enough.”

The ANIMATING IDEA, DR. RIZKALLAH SAYS, was to change the paradigm “from ‘they make more by spending less’ to ‘they make more by spending more on patient care.’ ”

The American Dental Association, dentists and dental organizations around the country lined up behind Question 2. The insurance industry fought back. Many dollars—including more than $3 million of Dr. Rizkallah’s own money and $5.5 million from the ADA, as well as millions more on the insurance industry side—were reportedly spent. The people of Massachusetts voted.

It was a rout.

Question 2 prevailed, 71.6 percent to 28.4 percent. The revolutionaries had launched the crates of tea into Boston Harbor.

“It is a sea change, because it changes the status quo of the business design that has been untouched since the 1970s and ’80s,” says Chad Olson, the ADA’s director of state government affairs.

Mike Adelberg, executive director of the National Association of Dental Plans (NADP), the dental-benefits trade organization, complained in an article published on his company’s website that the Massachusetts vote was taken “without the benefit of a legislative process in which professionals consider pros and cons. . . . Now, a handful of state bills suggest the Massachusetts mistake could be repeated. NADP believes the Massachusetts public ballot language is bad public policy that will not achieve intended consumer and dental community benefits.”

As Adelberg suggested, the Bay State may represent just the beginning of this revolution. Dr. Rizkallah, the ADA and others are now pushing for more states to adopt a formal medical loss ratio for dental care and for the federal government to act.

“There’s a buzz now, and it’s just a matter of time,” Dr. Rizkallah says. “You keep hitting that wall, and all of a sudden, you can knock that thing down.”

If successful, the Boston Teeth Party and other like-minded groups around the country will change the way almost everyone pays for and receives dental care. Changing the law in one state is of course a vastly different task from changing it in all 50. What happens now? Let’s drill down.

ANY DISCUSSION about dental insurance must start with an understanding of what it is and is not.

“People walk into my office every day and say, ‘I have dental insurance,’ and I say, ‘Not really,’ ” says Dr. Mark Vitale, an Edison, New Jersey–based dentist who chairs the New Jersey Dental Political Action Committee. “There’s no such thing as dental insurance.”

With a typical major medical insurance plan, the patient pays premiums—as well as copayments and a deductible—but may receive benefits that have no maximum no matter how much care is provided. If you’re hospitalized for a serious illness or injury, your insurance likely will cover a significant portion of that bill, the carrier’s payments rising alongside the treatment’s costs.

Dental insurance doesn’t work that way. You’re paying into the system, but the benefits you receive—like, perhaps, some of your teeth—will be capped. A plan’s annual maximum often is $1,000 to $1,500. Some plans may reach $2,000 annually, but few have no maximum, so if you’re in a serious accident or otherwise require, say, $10,000 worth of dental work, your insurance will not cover any expenses beyond the plan’s cap.

Dr. Vitale notes that in New Jersey, a crown is priced at about $1,600 on average, and most dental insurance plans pay out 50 percent before the maximum is reached. So one crown will cost you $800 out of pocket, with $800 covered, but if you need three crowns, and your insurance is capped at $1,500, you’ll owe $3,300 of the $4,800 total.

That’s why the ADA’s Olson likens so-called dental insurance to “a gift card.” Once you hit your limit, you’re on your own, and the more you need, the less proportional benefit you receive.

“Dental insurance isn’t dental insurance,” Dr. Vitale says. “It’s a reimbursement plan or a benefit plan.”

“Private insurance and third-party administrators of Medicaid programs are basically the Greek hydra, the multiple-headed dragon. You gotta hit them over there, but then they creep up over here and bite you. At some point I realized the only way I’m gonna kill this hydra head is to kill the system.”

In its online “History of Oral Care,” Delta Dental traces the first dental plans to 1954, when the International Longshoremen’s and Warehousemen’s Union and the Pacific Maritime Association (ILWU-PMA) requested dental benefits for its workers and their children. In response, the Washington Dental Service, the Oregon Dental Service and the California Dental Association Service were born, with the California organization eventually becoming Delta Dental of California.

“The whole concept was to create access to care for individuals who felt they couldn’t go to the dentist because they couldn’t afford it,” Dr. Vitale says.

“It served a great purpose when $1,500 could buy you great dental care.” But since he began practicing 40 years ago, he says, the typical $1,000 to $1,500 annual maximum has not changed, while premiums and procedure costs have risen dramatically. Olson says the standard $1,500 annual benefits ceiling has been in place since the 1970s, when it should be up to about $15,000 by now.

What’s more, Olson, Dr. Rizkallah and others argue, those annual maximums give the dental benefits carriers something that other medical benefits companies lack: predictability. Other medical insurers can apply their most sophisticated analytics to the industry, but they don’t truly know how many claims will be filed within a given year and what their total costs will be. “Maybe one year ER are visits up 30 percent,” says Dr. Andrew Chase, past president of the Massachusetts Association of Orthodontists (MAO) and current chair of its Public & Professional Relations Committee. “Medical insurance doesn’t necessarily know the limit.”

By contrast, a dental-benefits provider can theoretically look at the number of customers in its system, multiply that by the dollar limit on each plan and calculate the absolute maximum that it could pay out (but likely won’t, because not everyone hits the limit) for patient care each year. Dr. Chase argues that the medical loss ratio for dental benefits should be higher than that for non-dental medical insurance because dental-coverage companies, unlike medical insurers, have no risk to manage. Question 2 set Massachusetts’ dental MLR at 83 percent, five points lower than the state’s medical MLR, but Dr. Chase speculates that after the data on costs and benefits under the new system is collected, “we believe the dental MLR will be closer to 90.”

A public affairs executive at Delta Dental of Massachusetts said the company would not comment for this article.

The NADP’s Adelberg says that some dental-benefits companies do offer no-maximum plans now—he provided a chart showing that 9 percent of commercial dental PPO plans in 2021 had no maximum—but notes that most consumers choose not to buy them. “The no-annual-max products are generally not being selected because people would rather save the money on the monthly premium,” he says.

He further argues that the differences between dental and medical insurance are a reason not to impose a medical loss ratio on the dental world. “Dental plans and health plans are not all that similar, so to assume that you have a regulatory construct, MLR, that can be ported over into dental without any significant modification is bad public policy,” he says. “It’s a mistake.”

Part of the problem, he says, is it doesn’t make sense to take a “one size fits all” approach regarding the administrative costs of, say, a $25 dental HMO and a $600-a-month medical plan. “Too many of these costs are fixed or quasi-fixed, and there simply is no ability for a low-premium plan to operate at the same loss ratio as a high-premium plan,” he says. “Regulators have understood this for decades.”

In his column on the NADP site, Adelberg objected to the MLR distinction between “good costs” (paid claims) and “bad costs” (administration) and the prospect of companies offering rebates if the good costs don’t reach an adequate level. “Dental plan premiums are tiny (less than 10 percent of medical plan premiums), so any rebates will be tiny,” he wrote. “The administrative cost of distributing the rebates might exceed the value of the rebates.”

Dr. Rizkallah doesn’t buy NADP’s figures or arguments, and he says so bluntly: “The insurance industry is sociopathic.”

DR. RIZKALLAH, 48, operates six orthodontic practices in the Boston area and has a long history of conflict with MassHealth, which oversees the state’s Medicaid and Children’s Health Insurance Program (CHIP). He and the Medicaid Orthodontists of Massachusetts Association (MOMA), an organization he created, first sued the state’s attorney general in 2014 over MassHealth’s changes to the state’s Medicaid program that, he argued, set an unreasonably high threshold for children to receive orthodontic care. MassHealth was reported to have settled the suit in 2016, reinstating its former standards and paying Dr. Rizkallah, who funded the lawsuit, $50,000 in legal fees (which he reportedly donated to the National Health Law Program, a D.C.-based litigation and advocacy group).

Another MOMA/Rizkallah suit reversed 2017 MassHealth regulations calling for doctors to bill in advance for treatments yet to be delivered. A third suit came in 2020 as Dr. Rizkallah and MOMA sought to reverse a MassHealth shift in orthodontic diagnostic terms that, he felt, would cause poor children to receive less-desirable diagnoses than well-off children. A December 2020 court injunction halted that change.

SWITCHING FROM DEFENSE TO OFFENSE, the Massachusetts attorney general’s office sued Dr. Rizkallah in 2021, accusing him of keeping children in braces for longer than medically necessary, fraudulently billing for mouthguards, submitting millions of dollars in false claims to MassHealth and, in an amended complaint, illegally charging patients for missed or canceled appointments. He denied these charges, accused the state of retaliation and filed a defamation claim, which is proceeding despite the state’s efforts to have it dismissed.

“They’re going to end up going, ‘Let’s settle it,’ but the reality is I’m not settling it,” he says. (MassHealth did not respond to requests for comment.)

Amid these suits, he has decried the intertwining of MassHealth, Medicaid third-party administrator DentaQuest, insurance company Delta Dental of Massachusetts and its corporate parent, the not-for-profit Catalyst Institute. When 2019 tax forms showed that Delta Dental of Massachusetts contributed that $291 million to the Catalyst Institute while spending $177 million on patient care, Dr. Rizkallah sought to act again.

“Private insurance and third-party administrators of Medicaid programs are basically the Greek hydra, the multiple-headed dragon,” he says. “You gotta hit them over there, but then they creep up over here and bite you. At some point I realized the only way I’m gonna kill this hydra head is to kill [the system].”

That got the referendum campaign going. Dr. Andrew Chase of the Massachusetts Association of Orthodontists recalls: “Mo called me up one day and said, ‘Hey, I’ve got an idea. This is how the paradigm shifts. We provide an opportunity for them to be profitable when they’re spending money on patients instead of denying payments. The more money they spend on patient care, the more profitable the companies will be.’ ”

Eventually spending more than $3 million of his own money, which he says he has accumulated through real-estate investments and other means, Dr. Rizkallah set out to initiate a ballot question. Approval of Question 2 on the November 2022 ballot would not only establish the 83 percent medical loss ratio for dental plans but also require insurers to refund any surplus to policyholders and, perhaps just as important, mandate that insurers report publicly their data regarding their MLR, administrative costs and other financial information.

“I want to be able to create transparency so we could take that data and say, ‘This is their actual costs, and these companies file [taxes] as not-for-profit, but they’re wasting here, here, here, here, here,’ ” Dr. Rizkallah says. “Then you can take this information to a legislature in a different state, and you can say, ‘This is the real cost to insure.’ ”

“People walk into my office every day and say, ‘I have dental insurance,’ and I say, ‘Not really.’ There’s no such thing as dental insurance.”

He gathered some powerful teammates, including the ADA, which helped the referendum clear “a few legal hurdles,” Olson says, and ultimately contributed $5.5 million toward the $8 million it raised overall. Dr. Abe Abdul, president-elect of the Massachusetts Dental Society (see No. 13, page 32), pushed for his organization to back Dr. Rizkallah’s efforts and for other state dental societies to follow suit. “He worked outside organized dentistry, and I worked inside,” Dr. Abdul says. “At the beginning there was some skepticism—even in Massachusetts—in terms of getting this done, but once we moved past that, it was unstoppable. Because it was the right thing to do.”

In the end, 49 state dental societies supported Question 2 in Massachusetts, with many more dentists joining the cause. “It is very clear Dr. Rizkallah could not have done this without organized dentistry, and organized dentistry could not have done this without the work of Dr. Rizkallah,” Dr. Abdul says.

Dr. Chase, another member of the Boston Teeth Party, says the group wasn’t looking to reinvent the wheel but to apply principles already contained in Obamacare and Romneycare. “That whole concept that patients are taken care of first has been around for a long time,” Dr. Chase says. “The dental component of it was excluded.”

Question 2’s opponents included the Committee to Protect Access to Quality Dental Care and the Committee for Competitive Dental Plans for Consumers, which together reported $9.5 million in contributions, according to the Massachusetts Office of Campaign and Political Finance. NADP also commissioned a study by the Seattle-based consulting and actuarial firm Milliman that found that smaller insurance carriers would have more difficulty meeting the 83 percent MLR and might need to increase premiums by almost 38 percent.

“The products are priced by actuaries,” the NADP’s Adelberg says. “It’s just math.”

Dr. Rizkallah argues that the Milliman study wasn’t credible, as it relied on data that was provided by NADP and not independently audited or verified. Olson also disputes its key conclusion, noting that the state has oversight and can prevent insurers from “raising premiums extremely.” At the same time, he understands why the industry would defend the system. “That’s the structure that makes them money, they are very comfortable with it and they would like it to stay the same for all eternity,” he says. Yet, he adds, customers’ viewpoint is “ ‘Of course I want the vast majority of my premiums to go to my care. Why isn’t that happening already?’ ”

The dental-benefits industry’s efforts couldn’t overcome such an argument. “I have a sister in Massachusetts, and when I called her, I said, ‘You have an opportunity to vote on it,’ ” Dr. Vitale says. “She talked to her friends at work, and they all voted. It just shows the power of having a ballot question like this that’s pro-consumer.”

“The proponents of the ballot initiative had a big head start in public messaging,” Adelberg acknowledges. He notes the “the bumper-sticker simplicity of advocating for MLR” but adds that “anyone who looks closely at what goes into administrative costs will quickly discover that most administrative costs are for activities that we all agree a plan needs to perform.”

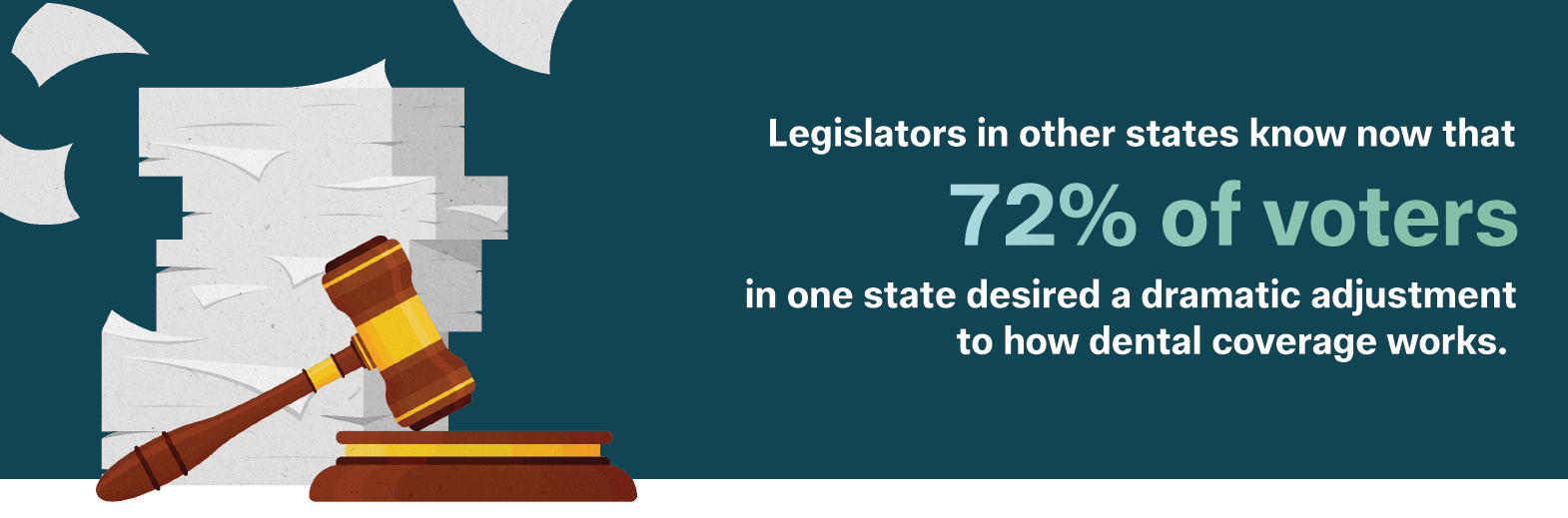

Question 2’s landslide victory gives the dental MLR cause “political equity,” in Dr. Rizkallah’s view. Legislators in other states know now that 72 percent of voters in one state desired a dramatic adjustment to how dental coverage works. But will that be enough to start the dominos falling?

Olson says the best-case scenario is for Massachusetts to serve as “a great launching pad” for the movement to spread. “We get a few states in the next couple of years to adopt this, and then it can be a streamroller.”

But most states do not allow an individual to introduce a referendum that would be binding after one ballot, and convincing legislatures to pass similar bills is more challenging, Dr. Rizkallah says. He notes that Oklahoma basically “copied and pasted” the Question 2 wording for a dental MLR bill, but it died in a tie vote in the state’s lower house in April. Rhode Island would seem a likelier bet—“we feel like we have a great chance there,” Olson says—but after a recent meeting with representatives there, Dr. Rizkallah says that effort may be difficult too, at least for now.

HE’S PINNING HIS HOPES on the data to be gathered over the next two years that will lay out how much money is being collected in premiums and spent on patient care and administrative costs. He expects these figures to make the case that the MLR has had a positive impact. “That data will then go to support effective legislation,” he says. “Right now I feel like it’s unlikely to get legislation passed without the data.”

Adelberg is counting on the data too—to have precisely the opposite effect. “For better or worse, the argument against a Massachusetts-style MLR law will get a lot stronger in January because people will see what happened,” he says. “There is a likelihood that premiums will go up the most in low-cost products, so the people who are the most price-sensitive, unfortunately, will see the largest price increases.”

Dr. Rizkallah is already looking beyond the states to effect more sweeping dental-coverage reform. “We’re actually going to be working to install that on a federal level,” he says. He predicts a national dental MLR will be passed within five years.

Olson and the ADA, meanwhile, continue to push for state-by-state action. “Our experience is it is tougher to pass things at the federal level,” he says. “We’re starting conversations with different offices at the federal level, but we don’t want to stand by and wait. If you’re a federal legislator, and your home state has this and it’s been very successful, it makes sense to pursue this for the country. It is an elegant solution to get this done in one fell swoop—but very difficult.”

Dr. Vitale predicts that the changes will go beyond the MLR into the nature of dental coverage itself, which will no longer be so different from other medical coverage. “I think over the course of the next five to 10 years. there will be a push to create actual dental insurance,” he says, with dental coverage folded into Medicare.

Dr. Abdul warns of one more possible obstacle standing in the way: divisions within dentists’ professional organizations. “I think anything that’s going to benefit health should be implemented, but I’m also not naive about the political process,” he says. “The biggest barrier to this at the beginning—and the biggest barrier moving forward—is, unfortunately, internal politics. I think the average dentist, the average provider, they all want this done 100 percent. We need to push this through.”

Amid so much uncertainty, all agree on this: The revolution that started with the Boston Teeth Party continues, with more battles to be fought. Says Dr. Rizkallah: “This is going to change the nation.”